Are emerging frequency benefits a simple symptom of an unprecedented economic environment that will inevitably mean revert, or will a changing economy lead to a secular shift?

Though a buy-in from Arch may still be the most likely outcome, there are potential alternative paths that could make the transaction less than smooth.

On Monday, the BLS released August CPI data which included -1.5% personal auto premium inflation. The figure is up from -1.9% in July, and a historic low in May of -14.3%.

Yesterday, the broker reported Q2 results that included positive data points and provided further evidence that more acute revenue pressures appear not to have materialized.

Earlier this week, Allstate announced the $4bn acquisition of National General, the latest step in its efforts to improve its omni-channel presence and compete for market share.

One popular theory of modern insurance is that improvements to financial accountancy rules and governance requirements under Sarbanes-Oxley have made the days of the “Little Black Books” obsolete.

On Friday Aon reported earnings with its highest organic growth in 15-years . The blowout report gave a point of contrast on two roads that diverged in large-cap broking.

Signs of stress in the small-cap Florida and other southern state primary markets continued this week as the shadow of rating agency downgrades overhangs the market.

Just a day after we wrote, "the board is the problem",that problem seemed to partially resolve itself, with Argo announcing the five long-tenured directors targeted for replacement by activist hedge fund Voce would be retiring at the firm’s 2020 AGM, including chairman Gary Woods.

There is an old saying that you should never ask a barber if you need a haircut. The same goes for financial advisors who get paid on activity rather than success.

There is an old saying that you should never ask a barber if you need a haircut. The same goes for financial advisors who get paid on activity rather than success.

Hanover Insurance Group reported operating income for Q3 of $2.31/sh, a 17% increase from $1.97/sh in the prior period and a beat versus consensus at $2.09.

American Financial Group reported core operating earnigns of $2.25p/sh, an increase of 3% versus $2.19p/sh in the prior year period and a hefty beat to consensus at $2.01.

Having just put an embarrassing activist campaign behind it, Argo finds itself facing yet more scrutiny over its executive compensation disclosures, this time from the SEC.

It's been an interesting few weeks at Greenlight, with several new disclosures on exec comp pointing to a likely sale, but some confusing counter-signals too.

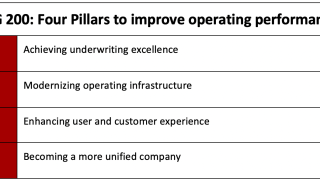

Taken alone, either of AIG's stated operating goals would represent an enormously bold target. Achieving both simultaneously within 2-3 years would be heroic.

Aon's D&O report gives a rare data-driven lens into the level of re-underwriting and risk appetite changes that are driving the tightening of capacity tightening in P&C.

One way to think about the ambitious build out of start-up (re)insurer Convex is an interesting test of the franchise values of specialty (re)insurers.

The new data points will likely continue to play into a narrative of "missing" price increases that have been widely discussed by industry participants but do not appear to show in industry pricing surveys.

We have previously written that a rationally competitive AIG could be the most important secular change to the US commercial P&C industry structure in a generation. As such, the firm’s Q1 results and earnings call will likely face even more scrutiny than normal.

Heading into earnings, our primary research leveraging an extensive network of industry contacts made clear to us that there is real “fear” in many pockets of P&C market leading to significant dislocation and re-underwriting actions in localized segments of the market.