Yesterday, WR Berkley reported second-quarter earnings, posting an underwriting profit in spite of elevated catastrophes and significant losses from Covid-19.

The carrier’s May results continued to display the multiple moving pieces resulting from the Covid-19 crisis, with loss ratios low but appearing to be heading back up, but elevated expense offsets.

May CPI data included another downward spike in auto price inflation driven by declines in accident frequency, with countrywide lockdowns related to Covid-19 leading to rebates.

As fundraising accelerates, we believe that capital formation coming in the front door as equity capital must be viewed in the context of alternative capital leaving through the back.

Willis’ Q1 commercial lines pricing survey showed a 6% rate increase, flat from Q4 and higher than all other 2019 quarters as large accounts recorded double-digit increases.

Lemonade published its S-1 on Monday, kicking off its IPO. We review three key discernable questions on what we assume is a business model hidden within hundreds of pages of Silicon Valley buzzwords.

Are the elements needed for a sustained hard market in play? Not so long as capital is knocking the door down to get into the market at the merest sniff of opportunity.

RenRe announced a ~$1bn share issuance yesterday, its first public raise since 2001. We think the move may challenge a decade-long intellectual orthodoxy of the “tipping point”.

Preliminary data for May suggests auto frequency is down about 43%. The figure is close to the ~50% benefit we observed in April, but nevertheless shows a lessening of the frequency benefit.

P&C company stocks outpaced the gains of the broader market in May, suggesting a relief rally on the back of more positive call commentary at Q1 earnings and optimism around the pricing environment.

With pricing accelerating and talk of a once-in-a-generation hard market, the P&C market continues to be talked about as entering a period of peak opportunity.

Allstate has extended its 15% premium rebate by a month. Notably, a few other companies have also added to their original rebates including State Farm, USAA and American Family.

It was clear to us by early March that 2020 would likely be a “prove-it” year for the remaining Bermuda independents, and suddenly these companies have much more to prove.

The carrier’s April results displayed multiple moving pieces from the Covid-19 crisis, including lower loss ratios in personal and commercial auto, but also a higher expense ratio and lower growth.

Yesterday marked the start of the first significant activist campaign targeting a public insurance company in 2020, following a tipping point last year with the ouster of Argo CEO Mark Watson by Voce.

The “empty-street” economy has left auto-exposed names in a relatively favorable position – so much so that they have been returning premiums to clients.

New data from Aon on D&O pricing in Q1 shows continued acceleration of rate increases.That said, we still see the true story as more balanced, with excess pricing changes distorting headline figures.

On Tuesday, the BLS released March CPI data that included a downward spike in auto price inflation to -6.2%, driven by declines in accident frequency related to country-wide Covid-19 lockdowns.

Covea announced it would no longer be acquiring PartnerRe. The move seems likely to torch its reputation as a potential merger partner and will present challenges for its purported strategic goals.

The company released its Q1 earnings, which included a 0.3pt improvement in its combined to 92.2%, as it reaffirmed its FY2020 guidance of $6.45-$7.25 in operating EPS.

On earnings calls, executives at the major reinsurance underwriters signaled a greater likelihood that losses on the sector would be contained, offering a juxtaposition to primary and retro markets.

The turnaround effort at Third Point Re took hold, after the company reported strong results that included its best underwriting result as a public company and continued favorable development.

UPC investors breathed a sigh of relief as the Floridian returned to underwriting profitability after reserve development turned favorable and underlying results improved.

A previously reported Covid-19 loss of $150mn dampened underwriting profitability, though the remaining underwriting results were roughly in line with the year before.

The hedge fund reinsurer reported a slight underwriting gain and a sharp reduction in written premiums, overshadowed by a $35mn investment loss in the David Einhorn-managed portfolio.

Alleghany reported an underwriting loss after its reinsurance segment took a $153mn charge tied to Covid-19-related losses. Underlying margins at TransRe and RSUI improved overall.

The New Jersey-based carrier lowered full-year 2020 guidance on both underwriting and net investment income based on expectations of top-line and alternative investment income pressures.

Tuesday’s call included an interesting shift in tone from AIG CEO Brian Duperreault, who suggested the company would “continue to look at” the possibility of a break-up of P&C and life.

The firm just missed analyst estimates after reporting a $65mn Covid-19-related loss in its mortgage segment that accompanied a higher cat loss total in general, causing operating earnings to fall.

Earnings at Axis fell as the company reported $300mn in cat losses – including $235mn stemming from the Covid-19 pandemic – as the carrier continued to show strong underlying improvement.

AIG will report earnings tonight and face investors tomorrow, and we see big strategic questions hanging over it on (a) AIG 200, (b) its capital allocation strategy and (c) its market sensitivity.

Yesterday, National General discussed Q1 results which included operating EPS of $0.91, up 18.2% YoY, and a headline combined ratio of 87.8% compared with 89% last year.

The JRVR management team detailed for analysts why it expected its Covid-19 exposure to be minimal, though it expects the fallout from the virus to hit the company’s top line in the second half.

Preliminary data for April suggests auto frequency is down around 50%. We expect this could put pressure on for more/bigger premium rebates, and potentially add liquidity stress to intermediaries.

Markel held its quarterly earnings call yesterday, during which it hit on a number of topics, including outlining for analysts the nature of the company’s pandemic losses.

Management struck a bullish tone as it outlined expectations of capped Covid-19 losses while asserting that lower claim frequencies would likely benefit the loss ratio more than falling premiums.

On its quarterly earnings call the Floridian insurer updated investors and analysts on how it has responded to the Covid-19 crisis and disclosed $50mn of Irma reserve development.

Cincinnati’s management team covered a broad range of topics on its earnings call yesterday including potential Covid-19 exposure and steps taken to mitigate customers’ cash flow pressures.

Benign frequency due to fewer miles driven in personal helped offset a weaker underlying loss ratio in commercial driven by one large fire loss and an unquantified Covid-19 loss reserve.

After a surprisingly positive start, new data points emerging from Q1 earnings are skewing negative. In fact, the drip-drip of bad news is starting to become a stream.

P&C companies likely face dissent on executive pay at upcoming AGMs amid deteriorating shareholder sentiment in the financial sector and a growing trend of executive pay cuts during the Covid crisis.

The second day of P&C earnings played out with more of the “leaning in” to negativity we had been expecting, and led to investors punishing the stocks of Chubb and RLI.

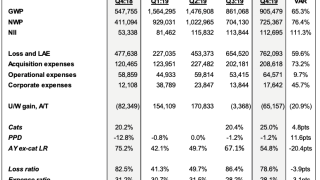

Berkley missed analyst estimates as underwriting income fell, primarily as a result of a $67mn charge the company took in anticipation of losses stemming from Covid-19.

Early reporters eased the tension with strong Q1 operating trends and some optimistic commentary on BI exposures. That said, the level of uncertainty remains high and unchanged by new disclosures.

Reinsurance renewal largely completed without interruption; reinsurers achieve rate improvements on loss-impacted programs, limited fallout from covid-19; June renewal onward expected to be a different story

With Q1 results kicking off on Tuesday with Chubb, Travelers, WR Berkley, and RLI, we see the set-up in P&C as skewed to the downside for the foreseeable future.

Recent news flow from Hiscox and QBE highlights some of the risks of investing in insurance companies at a time of crisis, even if valuations look “cheap” and your time horizon is long.

The BLS released March CPI data that included a spike in auto price inflation to 1.1%. We expect this is likely to prove an aberration given the change in loss-trend drivers in recent months.

Through its ability to apply rapid response stress tests on the entire P&C market, AM Best has an asymmetrical advantage over other commentators when it comes to real time market-sourced information.

Progressive included a 20% rebate for commercial lines customers with BOP and GL policies – potentially the first indication of rebates spreading from auto to small commercial customers.

Geico has raised the stakes in the arms race on customer rebates. Unlike other carriers to date, its plan is structured to more explicitly motivate retention, attract new business and protect float.

Yesterday, Allstate and American Family announced a plan to partially refund personal auto premiums. We expect these to be the opening bids in a protracted battle with regulators.

Early-stage InsurTechs will likely face fundraising challenges and huge incentives to grow at any price to “prove the model”, while incumbent carriers are at a maximum point of disintermediation risk.

For all the focus on the potential tail risks from Covid-19, the most probable outcome is a period of benign frequency allowing carriers to catch up to trend, altering the near-term industry paradigm.

The carrier's rehabilitation in the hands of private equity house Apollo hit a stumbling block yesterday after ratings agency AM Best revised its rating outlook on Aspen to negative.

Despite monumental headwinds that are likely to otherwise temporarily bring M&A activity to a halt, Bermudian (re)insurer Sirius International announced on Friday its intention to pursue a sale.

We use AIG as a case study to illustrate the tension between pressure to buy back stock at accretive levels versus the second-order impact on long-term strategies that require high earnings retention.

For many companies with “pot-committed” strategies with competing capital demands, increased buybacks should be seen as capitulation and a risk to longer term strategy.

The stock price movements of Aon and Willis Towers Watson since their mega-merger was announced suggests investors are proceeding with caution ahead of possible shareholder and regulatory opposition.

Root has has been dependent on private equity and reinsurance – a source of capital in flux given the Covid-19 pandemic – to continue operating at its current growth rate.

As the pandemic unfolds, the mortgage (re)insurance market—a boon to the industry since the last economic crisis—is more exposed to the larger macroeconomic cycle than the traditional P&C business.

“I’m from the government and I’m here to help.” P&C stock movements suggest the market can’t decide if these are the nine most reassuring or the nine most terrifying words in the English language.

For Axis, an undersized player with a recent record of earnings pressure, the decline in its shares is likely to translate into nearer term constraints that could narrow its long-term paths forward.

Transformations in Argo’s corporate governance following the proxy advisers’ support for little-to-no change raises questions about the role such firms play in a complex business like insurance.

P&C valuations plummeted from a recent peak of 1.42x to 0.92x, the lowest since 2013. The “worst of all worlds” thesis we outlined recently not only looks highly likely, it now looks even worse.

Progressive released its February results with a challenging macro backdrop. Key figures included a 90.3% consolidated combined ratio and an LTM shareholder ROE of 26.4%.

Argo’s proxy filing unveils the depth of its past culture issues and raises questions on what the board knew, when it disclosed it, and how that shaped the terms of Mark Watson's departure.

The BLS released February CPI data which included a 0.3% personal auto premium inflation. While the figure is up from 0.0% the previous month, these levels of inflation have not been seen since 2007, and point to carriers competing strongly for growth.

Greenlight Re faced scrutiny on the lack of progress from its strategic review, combined with apparent reluctance from conflicted sponsors in acting aggressively in the shareholders' interest.

Aspen and Argo hang over the Bermuda market, offering a parable of potential consequences for the remaining Bermuda “independents” in a make-or-break year.

Floridian specialist HCI released results last night, reporting operating earnings of $0.76/sh that missed analyst estimates, alongside a bullish update on its acquisition of a book of business from Anchor and signs of rapid growth in its InsurTech unit.

AM Best downgraded the financial strength rating of Sirius International to A- from A yesterday following a maneuver by CMIG to block a rights issuance by the Bermudian carrier that has called Sirius’ independence and financial stability into question.

PartnerRe's union with Covea gave it access to primary risk, leaving the reinsurer better placed, but the two must still address cultural challenges and the issues PartnerRe has faced in recent years.

In its call with analysts, Universal revealed a $150mn rise in the company’s Irma gross loss estimate, to $1.4bn, representing a total increase of $400mn in the second half of 2019.

Sirius parent CMIG blocked a rights issuance by the subsidiary that would have diluted CMIG’s ownership stake, calling Sirius' independence and financial stability into question.

French mutual Covea and Bermudian reinsurer PartnerRe announced they had reached a memorandum of understanding by which Covea would purchase Partner for $9bn cash, plus a $50mn cash dividend.

Universal’s earnings were badly hit by a combination of reserve charges and the recognition of prior-year losses that totaled more than $100mn and pushed underwriting margins into much further negative territory than a year ago.

Heritage held its earnings call Friday, echoing comments from fellow Floridian FedNat that AOB-related claims had fallen substantially since reform enacted in the middle of last year.

Third Point attributed its recent turnaround to the transition to a more well-rounded “specialty” reinsurer focused on underwriting profit, and away from the float-generating strategy that marked its early days.

FedNat shed light on improvements in the Florida market following AOB reform, but emphasized the tort environment still presents problems and is driving the company to pursue growth outside the state.

Third Point Re posted a strong improvement in underwriting results last night, with the company’s ex-cat combined ratio hitting below 100% for the second consecutive quarter and for the year.

The Boston-based mutual insurer swung to a $299mn quarterly net loss from continuing operations as a $555mn reserve charge from liability, casualty, and specialty lines hurt results.

What can go wrong? Lower yields. Market-linked income under pressure. Rising loss costs. Mean reversion in personal auto and workers’ comp. Welcome to 2020?

The Floridian ended 2019 with another disappointing quarter that included lower catastrophe losses, offset by prior year development and a current accident year true-up.

AM Best issued a cruel blow to the sense of a new dawn at Argo with a ratings downgrade and a negative outlook, largely citing corporate governance concerns.

Argo kicked off a new era under new leadership as it looked to rebuild bridges with external stakeholders after a bruising 2019, hinting at a bold plan to “simplify, reduce and eliminate”.

Argo reported an operating loss of $2.15/sh, including a $114mn underwriting loss that was mainly the result of a $77mn reserve charge tied to its London, Bermuda, and European operations.

Warren Buffett’s conglomerate reported ludicrous headline net earnings, but with a less healthy story in insurance with lower favorable development and notable deterioration of results at Geico.

Swiss Re became the latest to disclose significant losses in its US insurance unit, citing higher-than-expected severity trends and a challenging tort environment.

Progressive reported solid January results, but its stock still under performed the market by ~3% on the day as it became the latest to face the pressures of meeting elevated expectations in auto.

Argo announced the widely expected permanent appointment of Kevin Rehnberg to the CEO position. It also announced that former Allied World CFO Tom Bradley had been made chairman of the board.

AIG followed an encouraging Q4 print with 2020 guidance that disappointed investors, appearing to push out its expected earnings recovery further into 2021.

Key themes from the Q4 call were additional detail on the recently announced reserve charge, market conditions, buybacks, and the purchase of French insurer Axeria.

Interim CEO Kevin Rehnberg begins his tenure in time-honored tradition when taking over a P&C company at a “challenging” time: reserve charges, impairment charges and higher loss picks.

The #1 broker’s proprietary pricing index showed an 11% rate increase as the firming accelerated in Q4 at all major global regions and lines of business.

Everest reported Q4 operating EPS of $3.20/sh, easily beating analyst estimates, albeit against a consensus that had the benefit of pre-announced cat losses.

The trend towards the “conglomerization” of reinsurance entities integrating into large insurance companies seems set to continue, with the likely acquisition of PartnerRe by French mutual Covea.

With Q4 earnings in full swing, there are two emerging issues in commercial lines: social inflation versus mean reversion, and expense ratio surprises.

Selective reported strong earnings in Q4, but with results partially offset by remediation work in its smaller E&S segment and a more competitive personal insurance market.

On Thursday we got a better look at broking trends, including slower growth at MMC, improved synergy guidance on JLT, and continued positive trends at AJ Gallagher and Truist.

CEO Albert Benchimol met the firm’s recent underperformance head on and acknowledged the company “did not deliver the financial results expected in 2019”.

E&S premiums across 15 US stamping offices nationally increased 19% to $37.5bn in 2019, while the same offices recorded a total of 4.9mn filings, a roughly 9% increase from the 4.4mn filings in 2018.

AIG’s decision to exit the surety market illustrates that the re-underwriting wheels continue to turn at the carrier as it looks to dampen underwriting volatility and move away from its previous “large-limits strategy”.

Brown & Brown's Q4 earnings release included improved organic growth of 5.2% that exceeded analyst expectations and the company’s own guidance of 2.9% telegraphed in Q3.

Brown & Brown reported Q4 earnings with improved organic growth of 5.2% that exceeded both analyst consensus as a strong performance in brokerage offset weakness in services.

On Thursday morning, Travelers reported EPS of $3.32 versus $2.13 YoY and a headline beat versus analyst consensus of $3.29, in part driven by low catastrophe losses (thanks to an aggregate reinsurance recovery).

New inflation data shows continued pricing declines and rising average severity. Margin pressures continue to build as the spread widens, and frequency remains the wildcard.

Progressive’s national footprint and best in class real-time data and analytics make it a reasonable proxy for the auto insurance market and a likely leading indicator for market-wide trends.

With Q3 results in, and (re)insurance markets in a state of flux, an ever clearer picture is emerging of what winning and losing looks like in a hardening market.

Amid an environment of rampant social inflation, one of the best indicators of risk is how much growth was written in problematic lines during the soft market years.

New inflation data shows continued pricing declines and rising average severity. Margin pressures continue to build as the spread widens, and frequency remains the wildcard.