-

The CEO said his company would be going on offense to accelerate book value growth while strong market conditions lasted.

The CEO said his company would be going on offense to accelerate book value growth while strong market conditions lasted. -

Earnings at the international non-life business also halve as EMEA operations swing to a 12.5bn yen loss.

-

The company shrank its gross premium writings in the quarter by 12% to $138mn.

-

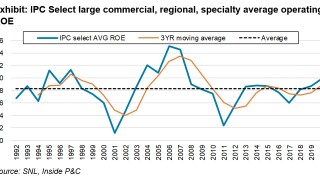

Will the latest iteration of re-underwriting and management change improve the return profile of one of the largest (re)insurance franchises?

-

The company was weighed down by a spike in mortgage claims, and higher cat losses in both insurance and reinsurance.

-

The company also said that it expects to grow underlying margins through underwriting actions that go beyond price improvement.

-

Pure pricing data suggested the D&O market kept taking rate-on-rate in Q4, while the policy restructuring and retention data showed early signs of peaking.

-

The (re)insurer had previously disclosed the $400mn reserve charge, largely connected to casualty reinsurance business from accident years 2015 to 2018.

-

The company improves its underlying loss ratio but takes a $19mn reserve charge in its commercial segment.

-

The second week’s reporters continued to build upon the theme of rate momentum likely translating into ROE expansion.

-

-

Executives reiterate the mid-single expansion guidance announced in March, despite growing organically by 1% in 2020.